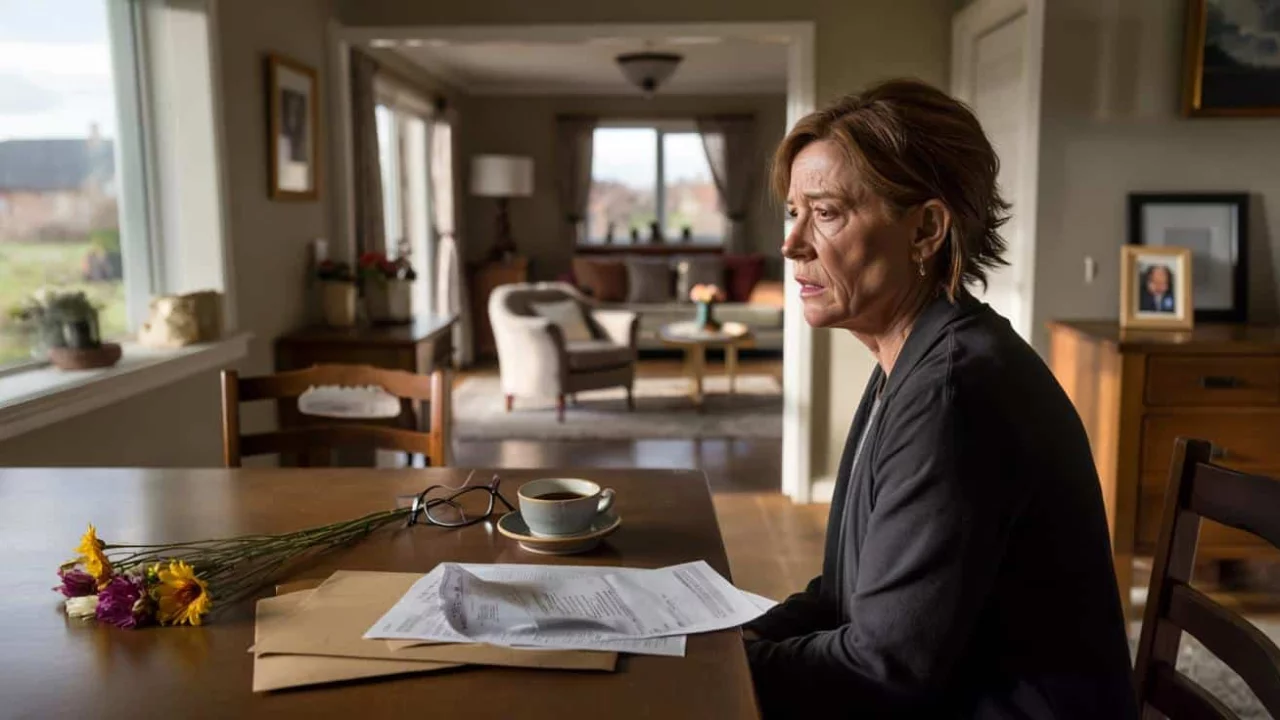

Sarah’s hands trembled as she opened the official-looking envelope three weeks after burying her husband of 24 years. Inside, a letter from HMRC demanding nearly £40,000 in inheritance tax on the modest terraced house they’d called home since 1998. The same house where she’d nursed him through his final illness, where his slippers still sat by the back door.

“I never wanted this house without him,” she told her sister through tears. “But apparently, the government thinks I’ve won some kind of lottery.”

Sarah’s story isn’t unique. Across the UK, thousands of grieving spouses discover that losing a partner doesn’t just mean emotional devastation—it can trigger a financial crisis they never saw coming.

When grief meets the taxman

Inheritance tax might sound like something that only affects the wealthy, but rising property values have dragged ordinary families into its net. The current threshold sits at £325,000, but when you add a family home worth £400,000 or more, surviving spouses can face bills that force them to sell the roof over their heads.

“We’re seeing more cases where people have to choose between keeping their home and paying a tax bill they can’t afford,” says financial adviser Marcus Thompson. “It’s particularly cruel because these aren’t people who consider themselves wealthy—they’re just homeowners who happened to buy in areas where prices rose.”

The rules seem straightforward on paper. Spouses inherit tax-free from each other, but when the surviving partner eventually dies, their estate—including the family home—gets assessed against inheritance tax thresholds. If you’re single when you die, your children or beneficiaries might face a substantial bill.

But there’s a twist that catches many families off guard. If the deceased spouse owned property in their sole name, or if couples weren’t legally married, the tax can hit immediately upon the first death.

The numbers that matter

Understanding inheritance tax means getting familiar with the key figures and exemptions that determine whether your family will face a bill:

| Threshold Type | Amount (2024) | Who Qualifies |

|---|---|---|

| Standard nil-rate band | £325,000 | Everyone |

| Residence nil-rate band | £175,000 | Leaving home to children/grandchildren |

| Combined maximum | £500,000 | Single person with qualifying home |

| Married couple maximum | £1,000,000 | When both allowances combined |

| Tax rate above threshold | 40% | On amount exceeding allowances |

The residence nil-rate band offers some protection, but only if you’re leaving your home to direct descendants. Step-children, partners you’re not married to, or close family friends don’t qualify for this additional allowance.

Here are the key factors that determine your inheritance tax liability:

- Total value of your estate, including property, savings, investments, and possessions

- Whether you’re married or in a civil partnership

- Who you’re leaving your assets to

- Whether your spouse used their full nil-rate band

- Any lifetime gifts made in the seven years before death

“The residence allowance sounds generous, but it’s not automatic,” explains estate planning solicitor Rachel Davies. “You have to actively plan to claim it, and there are income limits that can reduce it for wealthier families.”

Real families, real consequences

Behind every inheritance tax case is a family navigating loss while facing financial pressure they never anticipated. Take the Johnsons from Surrey, who discovered their £600,000 family home would generate a £110,000 tax bill when the surviving spouse died.

“We bought that house for £89,000 in 1985,” says their daughter Emma. “Mum and Dad were a teacher and a plumber. They weren’t wealthy by any stretch, but London house prices made them look rich on paper.”

The family faced an impossible choice: sell the home their mother wanted to leave them, or find £110,000 from other assets. They ended up selling, splitting the proceeds between three siblings who each got far less than their parents intended.

Similar stories play out in family kitchens across the country. Adult children discover that inheriting the family home means finding tens of thousands in cash within six months. Some remortgage their own properties. Others sell treasured family assets or take out loans against their inheritance.

“The cruelest part is that the tax is due six months after death,” notes Davies. “That’s barely enough time to grieve, let alone arrange complex financial solutions.”

The impact varies dramatically by region. In parts of London and the South East, even modest family homes trigger substantial inheritance tax bills. A three-bedroom terrace in areas like Clapham or Brighton can easily exceed £800,000, pushing families well over the combined thresholds.

Meanwhile, identical families in the North East or Wales might inherit similar-sized properties worth £200,000, facing no tax at all. This geographical lottery adds another layer of unfairness to a system that already feels punitive to grieving families.

“We’re creating a situation where your postcode determines whether your children can afford to inherit your home,” says Thompson. “That doesn’t feel like fair taxation—it feels like punishment for living in the wrong place.”

Some families get creative with solutions. Joint ownership arrangements, lifetime gifts, and trust structures can all reduce eventual tax bills. But these require forward planning and professional advice that costs money many families don’t have.

The government collects around £7 billion annually from inheritance tax, affecting roughly 4-5% of estates. But that percentage is rising as property values increase faster than the tax thresholds, pulling more ordinary families into the net.

For families caught in this situation, the emotional toll often exceeds the financial one. “It feels like the state is profiting from our grief,” one widow told us. “As if losing your life partner wasn’t enough—now they want a chunk of everything you built together.”

FAQs

Do I have to pay inheritance tax if I inherit my spouse’s house?

No, spouses and civil partners inherit from each other tax-free, but the tax may apply when the surviving partner eventually dies.

Can I avoid inheritance tax by giving away my house before I die?

Potentially, but you must survive seven years after making the gift, and there are rules about continuing to live in the property.

What happens if I can’t afford to pay the inheritance tax bill?

HMRC may accept payment by installments over ten years for property, or you might need to sell assets to raise the funds.

Does inheritance tax apply to all my possessions or just property?

It applies to your entire estate, including property, savings, investments, cars, jewelry, and other valuable items.

Can unmarried couples avoid inheritance tax?

Unmarried partners don’t get the spouse exemption, so inheritance tax may apply immediately on the first death if the estate exceeds £325,000.

Are there any legitimate ways to reduce an inheritance tax bill?

Yes, through lifetime gifts, charitable donations, pension planning, and using both partners’ allowances effectively, but these require professional advice.

Leave a Comment